The Personalization Gap Is a Loan Growth Gap

New research shows 89% of bank clients say offerings lack personalization. Community FIs that master data-driven prescreen marketing can capture borrowers fleeing impersonal experiences.

New research shows 89% of bank clients say offerings lack personalization. Community FIs that master data-driven prescreen marketing can capture borrowers fleeing impersonal experiences.

Prescreen marketing typically focuses on rates and credit limits. A shift toward outcome-based messaging—tying firm offers to member aspirations like homeownership or debt freedom—can unlock deeper engagement and differentiation.

Most banks have data and consumer permission to personalize, but remain stuck at broad segments. Learn why prescreen marketing offers community FIs a practical path to true 1:1 personalization.

Community FIs win loyalty in vulnerable moments, but those interactions rarely scale. Learn how precision prescreen marketing can replicate branch-level empathy across your entire membership.

By Devon Kinkead

From 2005–2025, deposit dynamics whipsawed: teaser-rate promotions pre-crisis, flight-to-quality in 2008–2009, a long low-rate lull, then 2022–2024’s rate shock and hot-money outflows. The consistent winner each cycle? Institutions that met customers at the moment of decision—not months later with a rate sheet. That’s the Micronotes thesis: detect, ask intent briefly, direct one clear path, and follow up automatically. Micronotes

History backs this. Heavy reliance on rate-sensitive or wholesale funds raises fragility; durable, relationship-driven core deposits stabilize earnings and liquidity. Empirical work finds that non-deposit/wholesale funding dependence elevates risk; banks that “rent” funding this way are more fragile through stress. Community banks, meanwhile, run with higher liquidity and greater dependence on core deposits, making a relationship-first retention model an advantage to press in 2026.

Instrument digital banking and core data to flag:

• Statistically exceptional deposits (windfalls, bonuses, asset sales)

• New/changed ACH payroll descriptors

• Brokerage outflows/rate-seeking patterns

• CD maturities and partial withdrawals

These are the “micro-moments” when balances are at highest risk of leaving—or most open to guidance. Micronotes’ deposit posts call out catching those signals as the foundation of retention. Micronotes

Why it works: Since the crisis, depositors’ preferences across deposit types changed—savings (flexible, liquid) surged while time deposits waned; the two have become more distinct economic choices. So you must identify which choice the customer is weighing right now and respond in kind.

Ask three human questions inside mobile/online banking:

Then present one recommended action (not a buffet): HYS for liquidity, a purpose-tuned CD/ladder for time-bound goals, or book-a-banker for complex sums. This is the core Micronotes flow. Micronotes

Why it works: Advice at the moment of intent changes outcomes—e.g., a windfall stays local instead of drifting to a brokerage sweep—without a rate war. Micronotes

Micronotes emphasizes framing deposits around life events and timelines, then making maturity choices easy in-app (roll, resize, step-out) to curb silent attrition. Micronotes

Why it works: Since 2008, the complementarity between savings and time deposits has weakened; customers treat them as distinct tools, so positioning must be crisp and purpose-led.

Route high-value cases to a small, trained team within hours; pass the micro-interview summary so the first call is consultative, not exploratory. Track “time-to-human” as a KPI. Micronotes’ guidance leans hard on compressing detection-to-help, not consideration-to-rate. Micronotes

Scorecard like a CFO:

These are the Micronotes “quality deposit” metrics that show durability and relationship depth, not just headline balance. Micronotes

Weeks 1–2: Instrument the signals (exceptional deposits, ACH changes, rate-seeking patterns) and deploy the 3-question micro-interview. Map each path to a single action (HYS, CD/ladder, or banker). Micronotes

Weeks 2–4: Publish one modernized offer + story (e.g., add-on CD or community-impact CD). Train front lines with the same plain-English script used in-app. Consistency reduces abandonment. Micronotes

Weeks 4–8: Launch, coach weekly on path-level conversion (parking-cash → HYS funded; ≈12-months → CD opened; “unsure” → banker booked). Micronotes

Weeks 8–12: Prove lift on exceptional-deposit retention, CD rollovers, primacy gains, and incremental margin vs. controls; shift budget from blanket rate spend to the signal-driven loop that’s compounding returns. Micronotes

You won’t out-rate megabanks and fintechs. You can out-value them—by catching decisions as they form and making the next step obvious, fast, and human when it matters. Community institutions already lead in core deposits and local trust; the Micronotes model turns that into measurable retention and primacy at a lower cost than rate wars. Start by turning on the signals, asking three great questions, and giving one great answer—every time. Micronotes

Sources: Micronotes deposits playbooks on signal-driven engagement, micro-interviews, and quality-deposit metrics; empirical findings on deposit type behavior and funding risk; and community-bank core-deposit strengths.

Governance note: The 2008–2010 policy response underscored how system fragilities outside traditional deposits can force drastic measures. A forward-leaning, relationship-driven deposit strategy is not just marketing; it’s resilience.

By Devon Kinkead

When Savana Morie’s recent article in Credit Unions Magazine highlighted Wright-Patt Credit Union’s transformative Pathways to Homeownership initiative, it struck a particularly personal chord for me. Having spent the first 18 years of my life in Dayton, Ohio, I’ve witnessed firsthand the challenges facing Northwest Dayton—the very communities Wright-Patt is working to revitalize.

But beyond the personal connection, this story represents something even more powerful: the intersection of mission-driven purpose and data-driven precision that defines modern credit union growth.

Wright-Patt Credit Union ($9.3B, Beavercreek, OH) has emerged as one of the two largest purchase-money lenders in the Dayton area, with more than half their mortgages going to first-time buyers. As President and CEO Tim Mislansky shared with Morie, “Affordable homeownership is one of the keys to financial success. When we can help members become homeowners, we can help them build wealth, strengthen families, and create lasting communities.”

That commitment is admirable—and it’s backed by a $1.3 million investment from the WPCU Sunshine Community Fund to construct 30 new homes in Northwest Dayton over the next three years. But here’s the question every mission-driven credit union must ask: How do you find the right people to fill those homes?

This is where prescreen marketing transforms theory into impact. Our recent (Sep 2025) Growth Opportunities Analysis for Wright-Patt Credit Union revealed something remarkable:

Within just 5 miles of Wright-Patt’s 40 branches, there are 172,328 credit-qualified individuals ready for mortgage opportunities—representing a potential loan volume of $35.8 billion.

Let me put that in perspective. While Wright-Patt is building 30 homes over three years through their Pathways initiative, there are over 172,000 qualified mortgage candidates already living in their branch network footprint. These aren’t random names—these are real people who:

| Criteria Definition | Rule Summary |

| FICO Score | Between 680 and 850. |

| Total number of debt counseling trades excluding collections | Equal to 0. |

| Total number of trades presently 30 or more days delinquent or derogatory excluding collections | Equal to 0. |

| Total number of trades ever 30 or more days delinquent or derogatory occurred in the last 12 months including collections | Equal to 0. |

| Total number of trades ever repossessed | Equal to 0. |

| Number of months since the most recent trade ever charged-off including indeterminates | No charged-off trades ever. |

| Total number of public record bankruptcies | Equal to 0. |

| Total number of trades excluding collections and student loans including indeterminates | Greater than or equal to 3. |

| Number of months since the oldest trade was opened excluding collections and student loans including indeterminates | Greater than 36. |

| Total number of non-medical collection trades | Equal to 0. |

| Total balance on medical collections | Less than or equal to $2,000. |

| Total number of first mortgage trades ever foreclosed including settled first mortgages | Equal to 0. |

Not all 172,328 will qualify for enough of a loan to meet market home prices so, the credit union should take market prices into account when designing the prescreen campaign ensuring that any such policy does not create a disparate impact under the ECOA or Fair Housing Act.

Traditional mortgage marketing casts a wide net and hopes for the best. Prescreen marketing does something fundamentally different: it identifies individuals who already qualify for your specific lending criteria before you ever reach out.

For Wright-Patt’s Pathways to Homeownership initiative, this precision matters even more. Director of Community and Social Impact Ivy Glover told Morie that the program includes a five-week homeownership readiness program, one-on-one coaching, and financial education sessions. That’s a significant investment of time and resources—which makes targeting the right candidates from the start absolutely critical.

“We didn’t just cut a check,” Glover explained. “We committed to making homeowners.”

Our Automated Prescreen™ platform analyzed 1,809,213 Experian records within 5 miles of Wright-Patt’s branch locations. After applying Wright-Patt’s underwriting criteria, we identified 723,188 qualified prospects across all loan categories.

For mortgage opportunities specifically, here’s what we found:

Once the program is executed, each prospect receives a personalized, firm offer of credit—not a generic “you might qualify” message, but an actual pre-qualified offer with specific loan amounts, rates, and monthly payments based on their individual financial profile.

One of Glover’s key insights in the article particularly resonates with our approach: “I wish we’d started the education piece sooner.”

This is where prescreen marketing creates a natural bridge between acquisition and education. When you reach a qualified prospect with a specific, personalized offer, you’re not starting a conversation from scratch—you’re answering a question they may have already been asking themselves: “Can I afford a home?”

For Wright-Patt’s target demographic in Northwest Dayton—where over 70% of residents rent and more than 40% are housing-cost burdened—seeing a concrete, qualified mortgage offer can be the catalyst that transforms “someday” into “now.”

Glover shared with Morie: “I tell my team all the time: Every drop makes a ripple, but some make a much bigger one. This is a big ripple moment.”

She’s absolutely right. But imagine if Wright-Patt could systematically identify and reach every qualified mortgage candidate in their branch network? What starts as a ripple could become a genuine wave of homeownership transformation.

Our analysis reveals opportunities across multiple product categories that support the journey to homeownership:

Each of these products plays a supporting role in the homeownership journey—helping members improve their debt-to-income ratios, build credit, and position themselves for mortgage qualification.

As someone who grew up in Dayton, I’ve watched neighborhoods transform—sometimes for better, sometimes for worse. The 2019 Memorial Day tornadoes that sparked the original Pathways to Homeownership initiative devastated communities I knew well.

What Wright-Patt is doing goes beyond lending. As Glover notes, “My teacher lived down the street; my doctor was two blocks over. One of the goals is to restore that sense of community and accountability where people know their neighbors and look out for one another.”

That’s the kind of community impact that makes this work meaningful. And data-driven prescreen marketing is the bridge that connects mission to execution—ensuring that every qualified member who could benefit from these programs actually knows they exist and can access them.

Wright-Patt still needs to raise an additional $2.75 million to complete Phase III of their housing initiative. But as Mislansky told Morie, “We believe this, along with continued fundraising and collective storytelling from all the partners, will lead to the additional funding needed to complete the next phases.”

Perhaps, if Wright-Patt can help more first-time homeowners at lower cost, it can funnel some of those savings into Phase III.

That storytelling becomes even more powerful when backed by data. When donors and partners can see not just 30 new homes, but 172,328 qualified opportunities waiting to be realized, the vision expands from a project to a movement.

Wright-Patt’s Housing Collective represents exactly the kind of cross-departmental, mission-driven thinking that defines successful credit unions today. But mission without mechanism is just aspiration.

Prescreen marketing provides that mechanism—the ability to:

For a credit union committed to making “more than half” of their mortgages to first-time buyers, the ability to systematically identify and reach 172,328 qualified mortgage candidates isn’t just a nice-to-have—it’s a strategic imperative.

Wright-Patt Credit Union is doing exactly what credit unions were founded to do: serving people of modest means and rebuilding communities from the inside out. Their $1.3 million investment, their five-week education program, their partnership with community organizations—all of it represents the best of the credit union movement.

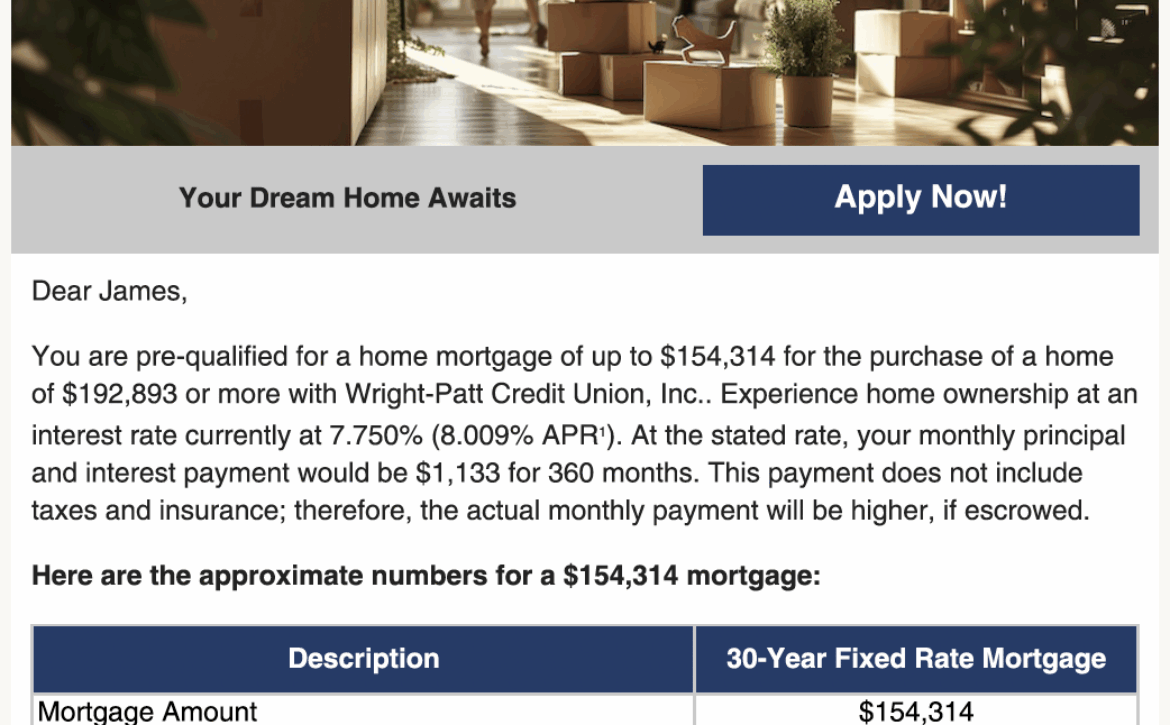

Micronotes’ role is to ensure that this incredible work reaches everyone who could benefit from it. That James, the single father in Northwest Dayton who’s been renting for years discovers he actually qualifies for a $154,000 mortgage. That the young couple making ends meet learns they could consolidate their high-interest debt and free up $261 per month. That the family dreaming of homeownership finds out their dream is actually within reach.

As Mislansky concluded in his conversation with Morie: “We believe this program can change lives, revitalize communities, and demonstrate what’s possible when mission-driven organizations work together.”

With 172,328 qualified opportunities waiting within just 5 miles of Wright-Patt’s branches, the question isn’t whether they can change lives—it’s how many, and how fast.

By Devon Kinkead

Banks talk endlessly about personalization. They invest millions in analytics, algorithms, and dashboards designed to “know the customer.” Yet, as The Financial Brand recently pointed out in Banks Are Failing at Personalization—Here Are Five Steps to Take Now, most institutions still fall short.

They’re not failing because of a lack of technology—they’re failing because their personalization isn’t anchored in monetary behavior.

At Micronotes, we believe the future of personalization is deposit-driven: spotting when money moves, identifying why, and responding in the moment. Because every large deposit is more than a number—it’s a story, a life event, and an opportunity to deepen a relationship.

The Financial Brand’s five-step framework—look beyond financial metrics, break down silos, earn trust early, deliver value first, and measure engagement—is sound. But viewed through a deposit lens, it’s incomplete.

Most personalization programs focus on digital behaviors: clicks, site visits, campaign responses. Those signals are weak compared to what’s already sitting in your core system—real-time deposit data.

A sudden $125,000 deposit doesn’t just happen. It could be from a home sale, inheritance, business liquidation, or retirement distribution. Each case represents a distinct customer need—investment guidance, mortgage payoff, cash management, or wealth transfer. And yet, too often, the bank does nothing. The deposit sits. Then it leaves.

That’s not personalization; that’s missed opportunity.

Personalization must start with the recognition that money in motion equals life in motion.

Micronotes’ Exceptional Deposits Detection identifies outlier inflows and triggers an automated digital conversation within hours—not weeks, or never. Our MicroInterview® technology engages the customer with short, relevant questions like:

Is this $92,374 deposit earmarked for a need within the next 12 months?

A branch and skip logic map sits behind this question to segment exponentially and it works because it’s behaviorally optimized:

-Behavioral Principle: Loss Aversion + Timing Effects

-Implementation: Copy frames missed earnings as a potential loss, delivered immediately after the deposit to exploit the fresh-start effect and completion bias.

-Expected Outcome: Nudges customers to either park funds in a higher-yield account or request wealth-management guidance before inertia sets in.

The responses reveal customer intent instantly, routing the right leads to the right banker. No cold calls. No guesswork. Just timely, contextual engagement rooted in data the bank already owns.

The Financial Brand suggests expanding beyond FICO scores and demographics. We agree, to some extent—but the most predictive signal of all is the deposit event itself. Track anomalies, not averages.

Personalization fails when data, marketing, and product teams don’t talk. In deposit retention, the critical bridge is between transaction analytics and product design. When an exceptional deposit hits, CD, wealth, and treasury teams should get an immediate, automated notification.

Trust begins when the bank shows up at the right time. A customer who just sold a home or received a business payout isn’t looking for generic messages—they’re looking for guidance. The window to act is small, often just days.

Don’t lead with a rate sheet. Lead with understanding. Ask questions. Then offer targeted pathways: “Would you like to protect these funds in a CD?” or “Would you like help investing part of it for growth?”

Value is delivered when engagement helps the customer make better financial choices.

Engagement is important—but retention is everything. The metric that counts most is how many exceptional deposits stay after engagement versus those that leave untouched. Our research shows that over half of large deposits exit within 90 days if no outreach occurs. That’s a measurable gap you can close—profitably.

A deposit-first personalization strategy looks like this:

This approach aligns personalization with the bank’s balance sheet. It’s not about more data; it’s about better timing.

The Financial Brand was right: personalization remains banking’s biggest unfinished project. But success won’t come from more dashboards or clever segmentation. It will come from meeting customers at the exact moments their financial lives change and earning their trust.

At Micronotes, we help banks turn deposit signals into dialogue—and dialogue into durable relationships. Because when your personalization strategy starts with the money, it ends with loyalty.

By Devon Kinkead

Mortgage originations may be stuck in a post-pandemic slump, but the path forward is hiding in plain sight: pair the digital muscle that trims cost and friction with the human guidance that turns complex borrowing decisions into lasting relationships. That is the core message of The Financial Brand’s recent feature on lenders who thrive in a volatile market by going “high tech with high touch.”(The Financial Brand) The same formula unlocks the even larger opportunity sitting on homeowners’ balance sheets—home-equity lines of credit (HELOCs).

1. Why the Dual Approach Works for Mortgages

2. The HELOC Market Is Even Hotter

Micronotes’ recent research calls 2025 a “HELOC renaissance.” Record equity (median > 50%), $1.2 trillion in costly credit-card balances, and 61 percent of owners locked into sub-6 percent mortgages create a captive, credit-hungry audience.(Micronotes) Adjust those debt figures for inflation and the headline “debt crisis” all but disappears—real leverage is roughly flat since 2020, leaving 28.7 million homeowners with true borrowing headroom.(Micronotes)

In other words, the same consumers struggling to qualify for a new mortgage may be perfect candidates for a well-structured HELOC.

3. Bringing “High Tech” to Home-Equity Lending

| Tech Lever | Mortgage Proof-Point | HELOC Application |

| Automated origination | PNC’s digital pre-qual sets expectations up-front (The Financial Brand) | Instant prescreen campaigns using Experian data flag equity-rich, high-utilization borrowers in minutes.(Micronotes, Micronotes) |

| Real-time status & e-closing | Huntington’s borrower dashboards reduce anxiety (The Financial Brand) | Remote online notarization and AVMs shrink HELOC funding cycles from 36 days to < 7.(Micronotes) |

| AI-driven personalization | Midwest Bank leverages fintech plumbing to scale advice (The Financial Brand) | Micronotes’ Automated Prescreen tailors messaging to the borrower’s actual savings from consolidating 20 %+ APR card debt into an 8 % HELOC.(Micronotes) |

Result: faster cycle-times, lower unit costs, and FCRA-compliant offers that land while competitors are still pulling credit files.

4. Keeping the “High Touch” at the Center

5. Strategic Payoff for Lenders

Bottom Line

The mortgage playbook proves that blending automation with authentic advice is the only sustainable way to serve today’s borrowers. Apply that same “high tech, high touch” philosophy to home-equity lending and you unlock a $25 trillion reservoir of value—for your customers and your balance sheet.

Volatility isn’t a signal to retreat; it’s a mandate to innovate. Lenders that harness data, speed, and human insight side-by-side won’t just weather the storm—they’ll own the next growth cycle.

By Devon Kinkead

When consumer debt is adjusted for inflation, the “debt crisis” narrative collapses. This creates significant opportunities for financial institutions to capture HELOC market share through intelligent, automated offer management.

The headlines scream crisis: consumer debt has exploded 28% since 2020. But this number tells a misleading story because it ignores inflation’s impact on the real value of money.

Here’s how inflation-adjusted debt analysis works: When prices rise by 20% over three years, a dollar today buys what 80 cents bought three years ago. So if someone borrowed $10,000 in 2020 and still owes $10,000 today, they effectively owe 20% less in real purchasing power terms.

Applied to the broader market, this reveals a stunning truth: when adjusted for inflation, consumer debt growth drops from 28% to just 3%. This means consumers aren’t drowning in debt—they’re maintaining roughly the same real debt burden they had three years ago.

Traditional debt-to-income ratios and leverage metrics become misleading during inflationary periods. Consider a homeowner who:

Nominally, their debt stayed flat. But in real terms, their debt burden decreased significantly while their earning capacity increased. This creates substantial borrowing headroom that traditional metrics miss entirely.

This inflation-adjusted reality coincides with three market conditions creating unprecedented HELOC opportunities:

Rate-Locked Homeowners: 61% of homeowners are locked into mortgage rates of 6% or lower, making refinancing unattractive and creating demand for alternative financing.

Rising Home Equity: Median home equity climbed from 35% in 2020 to over 50% in 2024—a massive pool of accessible capital.

Hidden Borrowing Capacity: The inflation-adjusted view reveals that 29.3% of homeowners with first mortgages and over 20% equity represent 28.7 million potential HELOC customers with genuine borrowing capacity.

Most financial institutions can’t capitalize on these conditions because their offer management operates on outdated assumptions and processes:

Meanwhile, online lenders capture market share by offering approval in minutes versus the 21-day industry average.

Automated prescreen technology transforms offer management from reactive to proactive by:

Real-Time Prospect Identification: Continuously monitoring equity levels, credit utilization, and inflation-adjusted debt capacity to identify optimal engagement moments.

Instant Qualification and Compliance: Validating regulatory requirements and performing credit checks in real-time rather than sequential reviews.

Intelligent Timing: Delivering educational content precisely when customers show behaviors indicating need—such as increasing credit card balances during inflationary periods.

In our recent webinar with Experian, we identified three critical challenges facing HELOC adoption:

Automated prescreen technology addresses these by educating customers about how HELOCs can optimize their debt structure, especially when inflation erodes the real value of fixed-rate debt while variable-rate credit card costs soar.

Phase 1: Data Integration

Phase 2: Automated Campaigns

Phase 3: Scale and Measure

The inflation-adjusted view of consumer debt reveals that borrowing capacity isn’t constrained by over-leverage but by outdated analytical frameworks and slow offer management processes.

With homeowners sitting on record equity levels and inflation actually reducing their real debt burdens, the HELOC opportunity is both substantial and time-sensitive. Financial institutions that understand this dynamic and can act on it quickly through automated prescreen technology will capture significant market share.

The question isn’t whether consumers can borrow more—it’s whether your institution can identify and engage them faster than the competition.

By Devon Kinkead

The banking industry stands at a critical inflection point where technology optimization meets unprecedented opportunities in home equity lending. Two recent industry reports—BAI Banking Strategies’ “Unlocking Value Through Technology Optimization” and Experian’s insights on HELOC Marketing Strategies in a Flat Rate Environment—reveal a compelling narrative about how banks can leverage digital transformation to capitalize on the $25.6 trillion in untapped home equity held by U.S. homeowners.

The current economic environment has created ideal conditions for HELOC growth. With 61% of homeowners locked into mortgage rates of 6% or lower and equally reluctant to sell their homes in the next decade, traditional mortgage refinancing has become less attractive. Meanwhile, median home equity has climbed steadily from 35% in 2020 to over 50% in 2024, creating a massive pool of accessible capital.

This “rate lock” phenomenon aligns perfectly with banks’ need to diversify revenue streams amid economic uncertainty. As the BAI report notes, banks are under pressure to optimize technology investments for competitive differentiation—and HELOCs represent a prime opportunity to do exactly that.

The intersection of these trends reveals a critical insight: technology optimization isn’t just about operational efficiency—it’s about market access and competitive positioning.

Traditional HELOC processes have been notoriously slow, taking 5+ weeks with dozens of documents and over 50% denial rates. Online lenders like Figure, Rocket Mortgage, and Spring EQ are capitalizing on this inefficiency by offering:

This directly aligns with the BAI report’s emphasis on “instant decisioning” and customer experience optimization. Banks that can leverage AI-powered underwriting, automated valuation models (AVMs), and remote online notarization (RON) can compete effectively with fintech disruptors.

Both reports emphasize the critical role of data analytics and AI. The BAI study shows that 75% of banks are exploring generative AI potential, while the Experian presentation demonstrates how data-driven segmentation can unlock HELOC opportunities:

Three key segmentation strategies emerge:

The typical HELOC borrower profile—761 FICO score, $140K income, 91% credit utilization—represents exactly the kind of customer that benefits from banks’ data analytics capabilities highlighted in the BAI report.

Experian identifies three critical challenges facing HELOC adoption:

These challenges directly map to technology solutions emphasized in the BAI report:

Banks need to bridge the gap between digital and personal service—exactly what the BAI report recommends. This means:

The BAI report’s emphasis on secure API connections and fintech partnerships becomes particularly relevant for HELOC marketing. Banks can leverage embedded finance solutions to:

Following the BAI report’s guidance on digital transformation, banks should prioritize:

Both reports emphasize data-centricity. Banks should:

Address the “PR problem” through technology:

Align with customer expectations for digital-first experiences:

The convergence of high home equity, rate-locked homeowners, and advancing fintech competition creates both opportunity and urgency. Banks that successfully integrate the technology optimization strategies outlined in the BAI report with targeted HELOC marketing will capture market share in one of 2025’s most promising lending segments.

The 29.3% of homeowners who have only a first mortgage and over 20% equity represent 28.7 million potential HELOC customers. With proper technology investments and data-driven marketing strategies, traditional banks can compete effectively against online-only lenders while deepening existing customer relationships.

The intersection of technology optimization and HELOC marketing opportunity represents more than just product promotion—it’s about fundamental business model evolution. Banks that view technology investments through the lens of market opportunity, rather than just operational efficiency, will be best positioned to capitalize on the $25.6 trillion in accessible home equity.

As both reports make clear, the future belongs to institutions that can combine the trust and stability of traditional banking with the speed and convenience of digital-first experiences. In the HELOC market, this combination isn’t just advantageous—it’s essential for competitive survival.

The time to “level up” is now. Banks that act decisively on both technology optimization and HELOC market opportunities will define the competitive landscape for years to come.