The Right Way to Measure AI ROI in Prescreen Marketing

Community banks and credit unions often measure prescreen AI investments the wrong way. Learn the function-focused framework that ties every campaign dollar directly to funded loan revenue.

Community banks and credit unions often measure prescreen AI investments the wrong way. Learn the function-focused framework that ties every campaign dollar directly to funded loan revenue.

By Devon Kinkead

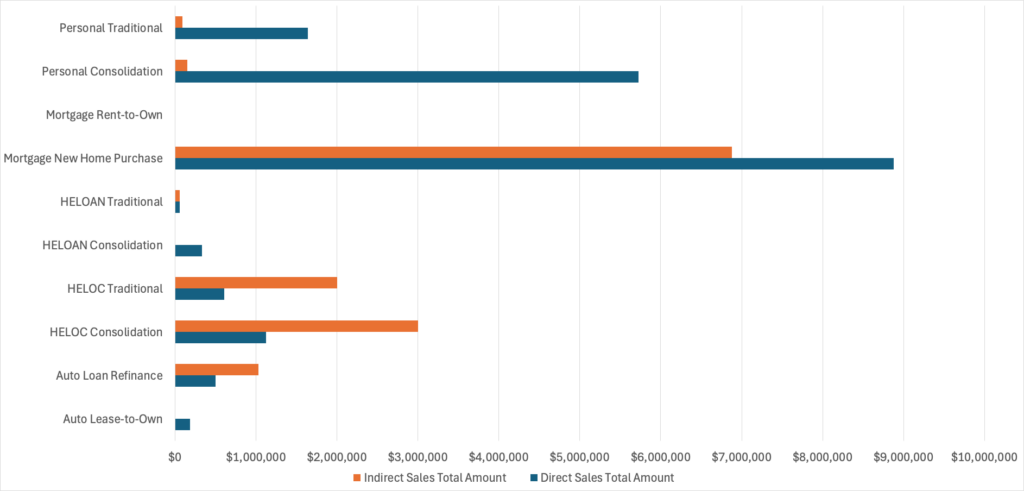

Vertically-integrated automated prescreen marketing systems are finding their way into community banking with obvious, and not so obvious returns. A review of 20 campaigns Micronotes’ customers ran reveals that 68% of the loan volume is in indirect sales; that is — an existing or prospective accountholder was offered one loan, like a HELOC, but originated a different loan, like a mortgage. Given the sheer volume of indirect loans, they represent an important but overlooked component of the return on investment analysis.

Direct Sales: These are the sales directly attributed to the prescreen marketing campaign. For example, a prescreen offer for a HELOC consolidation loan was made to a prospect on February 1st, 2024 and a HELOC loan was originated on February 24, 2024.

Indirect Sales: These are the sales indirectly attributed to the prescreen marketing campaign. For example, a prescreen offer for a HELOC consolidation loan was made to a prospect on February 1st, 2024 and a mortgage was originated on April 24, 2024.

Figure 1 – Direct vs. Indirect closed loan volume across different offer types. Note: no data for rent-to-own because this was a small scale test campaign.

Indirect sales vary by offer type, with indirect sales materially exceeding direct sales in HELOCs and auto loan refinancing and entirely absent in auto lease-to-own and HELOAN consolidation. Personal loan offers show relatively few indirect sales while mortgages show a significant fraction of indirect sales.

Summarily, return on investment computations must included indirect sales to accurately reflect the real net interest income generated by a prescreen loan campaign, particularly with HELOCs, auto loan refinance, and mortgages.

Understanding the real benefit of automated prescreen marketing requires a comprehensive dataset, excellent analytics, and a good working knowledge of probabilities. Micronotes has developed a vertically-integrated automated prescreen marketing tool that enables community financial institutions to launch campaigns and comprehensively measure the return on campaigns and understand the unique characteristics of each prescreen offer type. Armed with this knowledge, Micronotes’ customers continue to invest wisely to acquire new borrowers and expand wallet share with existing accountholders.

By Xav Harrigin-Ramoutar

In the evolving landscape of banking, the approach to acquiring new customers has significant implications for financial stability and growth. Traditionally seen as a marketing expense, customer acquisition is often constrained by rigid budget limits. However, by shifting this perspective to view it as an investment, community financial institutions can unlock sustained profitability and strategic growth. This article explores how this shift can positively impact financial planning and stability, especially by focusing on loan products and net interest income to offset the cost of customer acquisition (COCA).

Customer acquisition is typically viewed as a marketing expense, confined within the constraints of a pre-set budget. This perspective categorizes customer acquisition efforts—such as advertising campaigns, promotional activities, and outreach programs—as costs to be minimized. Consequently, when marketing budgets are exceeded, even successful campaigns are often halted. This limitation arises from a narrow focus on immediate expenditures rather than returns. By treating customer acquisition solely as a marketing expense, community financial institutions may overlook the substantial revenue these new customers generate through loan products and other financial services.

Viewing customer acquisition as an investment offers several benefits. It promotes sustained revenue growth by focusing on long-term customer value, particularly through loan products that generate interest income. Budget rejuvenation occurs when profits from new customers replenish and expand marketing budgets. This approach aligns with strategic financial planning, encouraging institutions to consider broader financial impacts and potential returns. By shifting to an investment mindset, community financial institutions can achieve greater financial stability, leveraging each new customer not just as an expense, but as a significant contributor to long-term profitability.

Viewing customer acquisition as an investment has several benefits that positively impact financial planning and stability:

Micronotes provides a compelling example of the benefits of treating customer acquisition as an investment. Community financial institutions can utilize Micronotes’ vertically integrated marketing automation technology to identify and target new customers for loan products. By focusing on these high-value prospects, financial institutions can successfully generate substantial net interest income that far exceeds the cost of customer acquisition (COCA).

Micronotes’ Growth Opportunity Analysis enables these institutions to size opportunity within the branch footprint and tailor their campaign strategies to meet specific needs and preferences.

Big data and analytics play a crucial role in demonstrating the ROI of customer acquisition as an investment. Micronotes’ vertically integrated marketing automation technology stack processes 230MM credit records per week and enables community financial insttitutions to know where every dollar of mispriced debt or lending opportunity is with creditworthy prospects in their operating footprint, then generate campaigns to acquire those prospective accountholders at a profit.

To shift from viewing customer acquisition as a marketing expense to an investment, institutions can adopt several practical steps:

These steps can help overcome budget constraints and encourage a strategic, investment-focused approach to customer acquisition.

Reframing customer acquisition as an investment can significantly enhance the financial planning and stability of community financial institutions. By leveraging marketing automation and adopting a long-term perspective, institutions can achieve sustained growth and profitability, transforming customer acquisition into a strategic asset.