Capturing the 2025 Auto Lending Opportunity: Looking at the Dashboard

By Devon Kinkead

The automotive finance landscape is experiencing a dynamic shift, and the latest Experian Q1 2025 State of the Automotive Finance Market report reveals compelling opportunities for lenders who can adapt quickly. With $1.6 trillion in outstanding auto loan balances and evolving consumer preferences, the market demands sophisticated, data-driven approaches to customer acquisition and retention.

The 2025 Auto Lending Landscape: Key Opportunities

Market Dynamics Creating New Opportunities

Experian’s data reveals several critical trends reshaping auto lending:

- Super Prime segment growth: The only risk tier seeing consistent year-over-year growth, representing prime opportunities for competitive lenders

- EV financing surge: Electric vehicles now represent nearly 10% of new purchases, with almost 60% being leased

- Banks regaining market share: Banks have returned as the largest lender type for used loans, barely edging out credit unions at 28.37% vs 28.24%

- Rising loan amounts: New vehicle financing averages $41,720, up 2.73% year-over-year

The Challenge: Standing Out in a Competitive Market

With captives (e.g. Ford Credit , GM Financial, Toyota Financial Services…) maintaining dominance in new vehicle financing (57% market share) and the landscape becoming increasingly fragmented, traditional marketing approaches are no longer sufficient. Lenders need precision targeting and personalized engagement to capture market share effectively.

How Micronotes Transforms Auto Lending Marketing

1. Precision Prescreen Marketing for High-Value Segments

The Experian report shows that over 83% of new loans are Prime+, indicating a concentration of opportunity in higher credit tiers. Micronotes’ advanced prescreen capabilities allow lenders to:

- Target Super Prime prospects who are driving market growth with highly segmented pricing tiers to boost win-rates

- Identify Lease to Own lending opportunities by targeting end-of-lease financially personalized prescreen offers

- Capture refinancing prospects as rates fluctuate across risk segments

2. Real-Time Market Intelligence Integration

With the automotive market showing nuanced trends—like the 7-point decrease in EV credit scores while ICE (Internal Combustion Engine) scores increased 2 points—timing is everything because:

Market expansion: Lenders who can identify and serve the expanding EV credit spectrum early will capture market share

EV market democratization: As EVs move from luxury/early-adopter purchases to mainstream adoption, there are new opportunities to serve near-prime and prime borrowers

Shifting risk profiles: The credit quality divergence between EV and ICE borrowers creates different pricing and targeting opportunities

Micronotes provides:

- Dynamic campaign optimization based on actual campaign results and market conditions

- Behavioral economics intelligence to capture customers with the right message

- Cross-selling opportunities leveraging existing customer relationships

3. Personalized Customer Journey Orchestration

The report reveals significant variation in financing preferences across segments. For example, luxury vehicles show different payment distributions than economy models. Micronotes enables:

- Segment-specific messaging for new vs. used vehicle buyers vs. refinance vs. lease-to-own

- Channel optimization across digital and traditional channels

- Geotargeting that adapts to branch footprint and individual market win-rates.

Strategic Applications for 2025 Success

Capturing the EV Financing Boom

With EVs representing 22.9% of all new leasing and showing unique financing patterns, lenders need targeted approaches. Micronotes can help:

- Develop specialized messaging for EV financing benefits

- Target EV buyers with competitive lease-to-own offers

- Automated prescreen marketing and optimization analytics

Competing in the Super Prime Space

As the only growing risk segment, Super Prime borrowers represent the most valuable opportunities. Micronotes enables:

- Proactive retention campaigns for existing Super Prime customers/members

- Competitive conquest strategies targeting Super Prime prospects with highly segmented pricing in the Super Prime credit score bands

- Rate-sensitive messaging optimized for credit-conscious borrowers

Leveraging Used Vehicle Market Dynamics

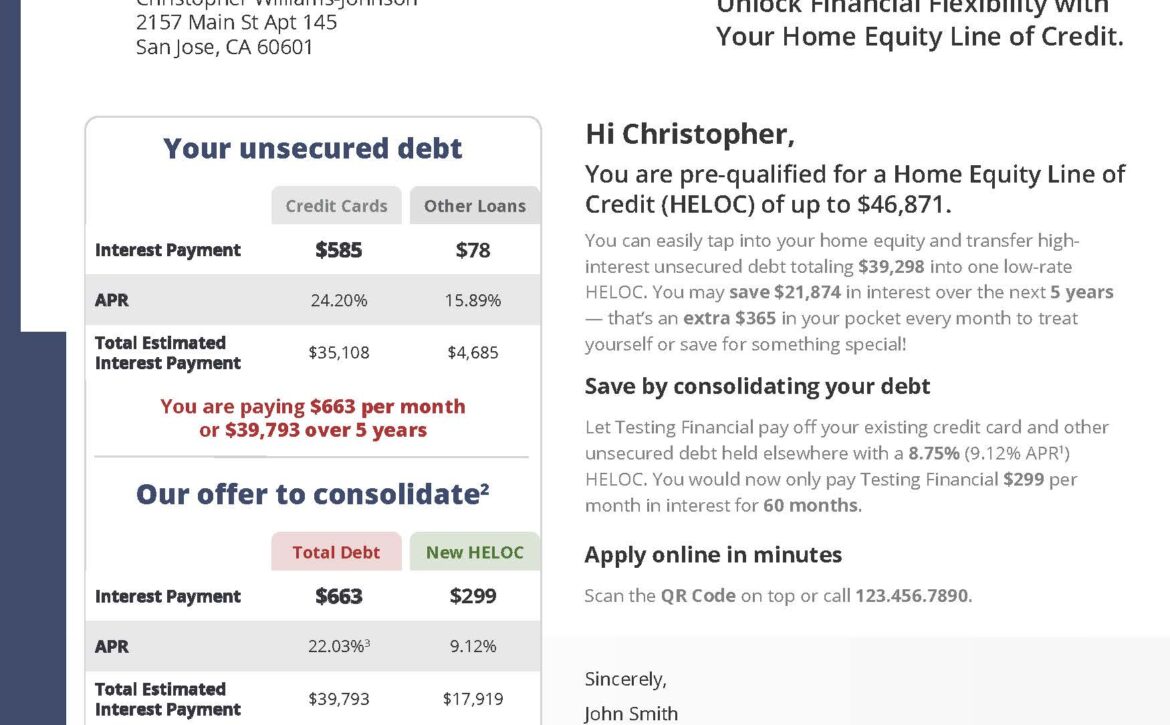

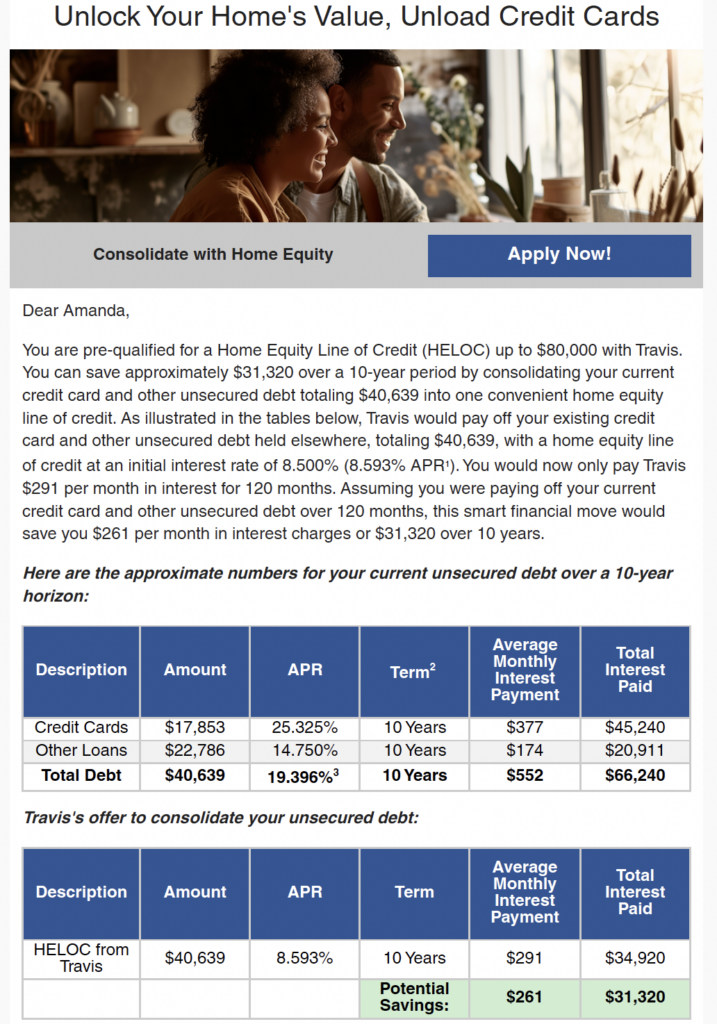

Refinancing mispriced auto loans is a great way to acquire new accountholders at net negative customer acquisition cost; particularly if they live in your branch footprint where the likelihood of converting those new borrowers to depositors is highest. Micronotes supports:

- Automated prescreen refinance campaigns with hyper-personalized firm offers showing individualized savings from refinancing

- Geographic targeting based on local market conditions

Looking Ahead: Positioning for Continued Growth

The Experian report shows that while overall balance growth has slowed to 1.43% year-over-year, strategic opportunities abound for lenders who can:

- Identify emerging trends early (like the EV financing surge)

- Target high-value segments precisely (Super Prime growth)

- Optimize pricing and positioning (responding to rate environment changes)

- Deliver personalized experiences at scale

Conclusion: The Future of Auto Lending Marketing

The automotive finance market of 2025 rewards precision, personalization, and proactive engagement. As the Experian data demonstrates, opportunities exist across all segments—from the growing Super Prime market to the evolving EV financing landscape.

Micronotes provides the technological foundation and strategic capabilities needed to capture these opportunities effectively. By combining advanced data analytics and optimization, personalized prescreen marketing automation, and omnichannel orchestration, lenders can achieve sustainable competitive advantages in this dynamic market.

The question isn’t whether the opportunities exist—the Experian data clearly shows they do. The question is whether your institution has the tools and strategies needed to capture them effectively.

Ready to transform your auto lending marketing strategy? Discover how Micronotes can help you capture market share in the evolving automotive finance landscape by scheduling a demo.