Why Prescreen Timing Beats Prescreen Volume for Loan Growth

Most community banks treat prescreen campaigns as calendar events, missing borrowers at their moment of need. A timing-first approach captures ready-to-act members before competitors do.

Most community banks treat prescreen campaigns as calendar events, missing borrowers at their moment of need. A timing-first approach captures ready-to-act members before competitors do.

Youth financial education programs create more than goodwill—they build a pipeline of future borrowers with known deposit behavior. Learn how to map today’s student accounts to tomorrow’s prescreen campaigns.

The first 45 days after account opening represent peak member engagement—yet most credit unions waste this window on exploratory outreach instead of precise loan offers. Learn why leading with prescreen-qualified credit offers transforms onboarding from nurture campaign to revenue engine.

Your best current borrowers may be teaching you the wrong lessons about new customer acquisition. Learn when familiar-market insights help prescreen campaigns—and when they mislead.

Rising credit card delinquencies reflect concentrated stress among already-struggling borrowers, not a wave of new defaults. Community FIs can pursue confident loan growth by targeting the right consumers with bureau-based precision.

New MIT research reveals why 84% of AI experts say responsible AI demands human judgment across the entire system lifecycle—not just final approval. For community FIs, this insight transforms how prescreen marketing should be designed and governed.

Inflation-adjusted wages grew just 0.1% last year while late-stage credit card delinquency hit a 20-year high. Community FIs have a narrow window to rescue struggling households—and grow loans—through strategic prescreen campaigns.

The latest Experian Automotive Market Trends Report for Q1 2026 is packed with data points that auto dealers and OEM marketers will pore over. But buried inside those vehicle registration tables and fuel-type charts is something even more valuable for community banks and credit unions: a detailed map of where your next auto loan is sitting right now, in whose driveway, and how urgently its owner needs a better deal.

Here is what the data tells lenders who know how to read it — and how automated prescreen marketing turns those signals into funded loans.

Experian reports 298 million light duty vehicles currently on U.S. roads, up from 293.5 million just twelve months ago. That fleet grew by 4.5 million units in a single year. More vehicles mean more outstanding auto loans — about $1.6 trillion — and more borrowers who financed during a high-rate environment and haven’t yet found a better deal.

The refinance opportunity alone is substantial. Auto loan refinance volume was up 11% quarter-over-quarter and 29% above Q2 2020 levels heading into this year, with average monthly savings to consumers of $47 to $71 per refinanced loan. With new car registrations in Q1 2026 down roughly 7% from the prior year — and the March spike widely attributed to consumers rushing to beat tariff-driven price increases — the used and refinance markets are where community lenders should be focusing their energy.

Not unlike the mortgage market, where millions of homeowners are locked into sub-6% first mortgages, the auto market has its own version of rate lock. Consumers who financed new vehicles in 2022 and 2023 — when rates were climbing sharply — are sitting on loans that many community FIs can now beat. The vehicles are depreciating, the rates were high, and the original lender has already collected the front-end profit. That borrower is winnable.

This is precisely the kind of opportunity that automated prescreen marketing is designed to surface. By scanning 230-plus million U.S. consumer credit records weekly through Experian’s Ascend Data Services, platforms like Micronotes can identify which members and prospects in your footprint have auto loans at rates above what you can offer today — and deliver a personalized, FCRA-compliant firm offer of credit before your competitors do.

One of the most striking findings in the Q1 2026 Experian report is the sharp acceleration of standard gas hybrid registrations. Gas/electric hybrids grew from 12.1% of new registrations in 2025 to 13.5% in Q1 2026 — a 4.1 percentage-point jump from full-year 2024. Meanwhile, BEV share declined again to 5.6%, and PHEV share is contracting. BEV = Battery Electric Vehicle (fully electric, no combustion engine), PHEV = Plug-in Hybrid Electric Vehicle (battery + combustion engine, can charge from an outlet)

What does this mean for lenders? Hybrids typically carry a price premium of $3,000 to $6,000 over their conventional counterparts. The Toyota Camry — now exclusively a full hybrid — commands that premium, as do the Honda CR-V hybrid and the Hyundai Tucson hybrid, all of which are top sellers in Q1. Higher transaction prices mean larger loan balances and greater opportunity for lenders offering competitive rates. Consumers who stretched to buy a hybrid in the last eighteen months and financed at or near peak rates are among the most attractive auto refinance targets in your market today.

Experian also reports that 72.6% of EV owners who returned to market replaced with another EV — loyalty to electrification remains high even as new EV adoption slows. These are engaged, financially active consumers who are making deliberate, research-driven purchase decisions. They respond well to personalized, data-informed offers — exactly the audience that prescreen marketing is built to reach.

New car registrations fell approximately 7% versus Q1 2025, but used vehicle registrations held steady at 10.1 million units for the quarter. The used market is enormous, persistent, and full of borrowers who financed through dealers rather than directly through a community financial institution. Many of those indirect borrowers are prime and super-prime consumers your institution would be glad to have — they just don’t know you exist.

Experian’s data on vehicles crossing state lines is another signal worth noting. In Q1 2026, 13.1% of luxury vehicle purchases and 9.3% of non-luxury purchases involved a buyer crossing state lines to complete the transaction. Digital retailing has broken the geographic loyalty that once naturally funneled buyers to nearby lenders. Community FIs cannot rely on proximity alone to capture auto loan volume. Proactive, data-driven outreach — a prescreen direct mail piece, a personalized email, a targeted digital banking notification — is increasingly the only reliable way to get in front of creditworthy borrowers before the dealership F&I office does (F&I = Finance & Insurance).

The Experian report notes that 34.9% of all U.S. light duty vehicles currently in operation fall into the aftermarket “sweet spot” — model years 2015 through 2021. These are vehicles aged out of manufacturer warranties, requiring more service spending, and approaching or past the natural replacement cycle for many households. Owners of 2015 to 2018 model year vehicles financed new are now largely done paying — or nearly so — and may be in market for their next purchase.

That clock is ticking toward your next wave of auto loan originations. Automated prescreen marketing is how you intercept those consumers at the moment of consideration rather than after they’ve already signed in an F&I office across town.

The Q1 2026 Experian data confirms what community lenders already suspect: the auto market is large, active, and full of qualified borrowers who would prefer a community FI over a megabank or fintech — if only they were asked. Prescreen marketing is the ask. Done well, it’s data-driven, FCRA-compliant, financially personalized, and delivered at exactly the right moment.

To find out how many auto loan refinance candidates are sitting in your branch footprint right now, order a free Growth Opportunities Analysis at micronotes.ai/growth-opportunities-analysis — it takes under two minutes.

Sources: Experian Automotive Market Trends Report Q1 2026

The basic structure of the blues is 12 bars. It’s 12 measures that relies on just three chords built off the 1st, 4th, and 5th scale degrees of a key. The batch prescreen blues is a progression of 100+ major tasks coordinated across multiple vendors and given all the delays and defects, can really bring a marketing and lending team down.

However, prescreen marketing remains the most effective tool a lender has for growing a quality loan portfolio. A pre-approved, personalized offer — “John, refinance your $40,639 in debt from 19.89% to 8.64% and stop overpaying $280 a month” — outperforms every other form of credit marketing because it is specific, credible, and FCRA-compliant. The borrower doesn’t have to wonder if they qualify. The lender doesn’t have to guess who to reach. The math is right there on the page.

So why do so many lenders leave so much of this opportunity on the table? The answer is usually the same: the batch prescreen blues.

A typical batch prescreen campaign involves more than 100 discrete tasks distributed across the lender’s marketing, lending, and compliance teams, a credit bureau, a mail house, a design agency, email providers, and often an additional data vendor or two. Each of those tasks is a handoff. Each handoff is a potential failure point. And together they generate three costs that compound quietly over time: labor, defects, and delays.

Labor is the most visible. Someone has to buy the list, brief the designer, write the compliance disclosures, transfer the file, check the proofs, coordinate the mail drop, and pull the response data when it trickles in weeks later. Then someone has to do it again for the next campaign. Marketing teams at community banks and credit unions are rarely large to begin with — and over the last decade they’ve gotten smaller. The operational overhead of batch prescreen is a significant and often invisible tax on those teams. Every hour spent on campaign logistics is an hour not spent on strategy, creative, or analysis.

Defects are harder to see but more expensive. In a multi-vendor, multi-step workflow, errors compound. A file transferred with the wrong segment filter. A compliance disclosure that didn’t make it into the final proof. A rate that was accurate when the creative was drafted but moved before the mailer dropped. In a manual process, each of these is a human failure waiting to happen — and the consequence isn’t just rework. A defective prescreen offer can trigger a regulatory problem under the FCRA, the ECOA, or UDAAP. The compliance risk in batch prescreen isn’t hypothetical; it’s inherent to any process where compliance is a final checkbox rather than an embedded control.

Delays are perhaps the most strategically damaging cost of all. A prescreen offer is time-sensitive by nature. The bureau data that identifies a qualified borrower reflects a credit profile at a moment in time. Rates change. Competitors are running their own campaigns against the same population. The lender who reaches a borrower first with a compelling firm offer captures the loan. The lender who takes eight weeks to execute a batch campaign — buying the list, designing creative, routing through compliance, queuing at the mail house — often arrives after someone else already has. Lead time isn’t just an operational metric. It’s a competitive disadvantage measured in lost loans.

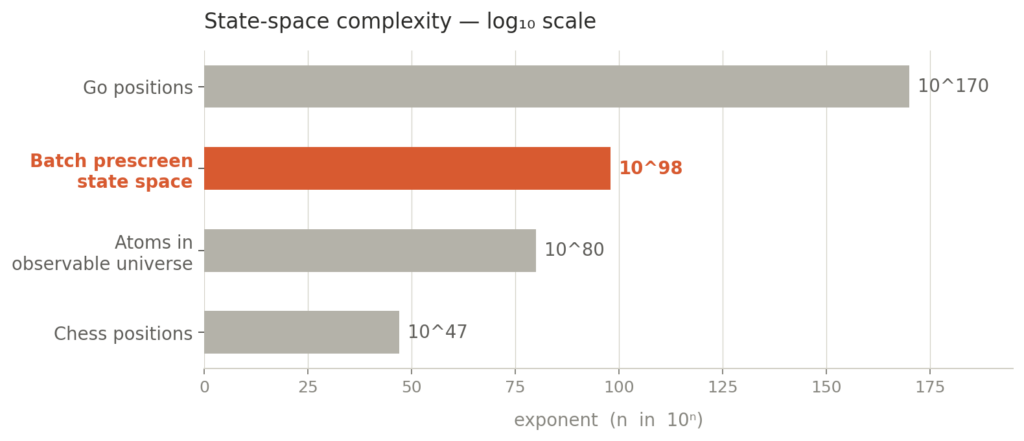

To get a sense of how complex this process is, here’s the math:

Each of 9 actors (marketing, lending, compliance, bureau, mail house, design, email, vendor ×2) has 7 possible states (idle, working, waiting, reviewing, blocked, defective, unavailable): 7⁹ ≈ 4 × 10⁷. Each of 100 tasks has 8 states (pending, in-progress, awaiting approval, approved, rejected, blocked, failed, escalated): 8¹⁰⁰ = 2³⁰⁰ ≈ 2 × 10⁹⁰. Combined: ~8 × 10⁹⁷.

The batch prescreen process produces a state space of roughly 10⁹⁸ — larger than the number of atoms in the observable universe. That’s not a metaphor for complexity; it’s the combinatorial math.

The practical implication: no human coordination system — no checklist, no project manager, no Slack channel — can reliably navigate a process efficiently with that many possible configurations. Any given campaign run is a single path through an incomprehensibly large space, and most defects and delays occur precisely because the actual state of the process (which vendor has which file, whether the rate is still current, whether the compliance disclosure is in the right version) is unknowable in real time.

Automated prescreen doesn’t reduce the number of tasks. It eliminates most of the state space by making transitions deterministic. When software controls the file transfer, the compliance check, the rate insertion, and the channel queuing, the number of reachable states collapses from ~10⁹⁸ to a small, auditable set. That’s why automation reduces defects and delays structurally, not just operationally — it’s a different class of process.

Automated prescreen — delivered as SaaS — doesn’t just do the same work faster. It restructures the work entirely.

In a properly automated workflow, underwriting criteria, rates, and campaign settings are locked in once. From there, the platform generates the selection file, submits it to the bureau, receives the prescreen file, assembles compliant personalized creative, queues the channel, launches, and posts results — including opened loans, NPV, and indirect sales — with no manual handoffs between steps. The seven tasks that used to require coordination across multiple vendors become a single orchestrated pipeline.

The impact on labor is immediate. Teams that previously spent weeks managing campaign logistics shift to reviewing results and adjusting strategy. The impact on defects is structural — compliance is embedded at each stage rather than verified at the end, which means the rate and disclosure problems that create regulatory exposure in batch workflows are caught and corrected automatically before anything goes to a borrower.

That’s not a coincidence. Speed and quality are usually in tension in manual processes. In automated ones, they compound together.

The campaign template behind a full prescreen program lists more than 100 individual tasks — file pulls, vendor briefings, proof approvals, transfer confirmations, tracking setups, attribution analyses. In a batch workflow, those tasks are distributed across people, vendors, and calendar weeks. Completing them requires coordination, version control, and organizational memory. Every person who touches the file is a potential defect source. Every week the campaign spends in queue is a week of loan volume waiting to close.

Automated prescreen collapses that task list into a managed pipeline. The institution still owns the decisions — underwriting criteria, channel selection, offer parameters — but the execution is orchestrated by software. The 100 tasks don’t go away. They happen faster, in sequence, with controls, and without distributing the burden across a dozen people and vendors.

The ROI case for automated prescreen is well-established. At $100,000 in annual platform cost, the breakeven is 33 additional funded loans — a conversion lift of just 0.03%. Institutions that achieve the typical realized lift of 0.10% generate $300,000 in incremental revenue, a 3x return before accounting for indirect sales, which on average represent 68% of total campaign loan volume.

But the more fundamental case isn’t financial. It’s structural. Batch prescreen was built for a world where automation wasn’t possible — where lists had to be bought, creatives had to be designed by hand, and mail houses had to receive files by FTP. That world is gone. The question isn’t whether lenders can afford to automate their prescreen programs. It’s whether they can afford not to — while labor costs accumulate, compliance defects wait to surface, and every week of delay hands qualified borrowers to a competitor who already made the offer. And we haven’t even started talking about post campaign analytics and optimization!

So stop singing the batch blues, you just can’t win in that sort of state space; switch to automated prescreen and let’s leave the blues to the musicians.

JD Power data reveals soft churn outpaces hard churn 2:1—your members are fragmenting relationships, not leaving. Prescreened credit offers can recapture wallet share before fintechs do.