Navigating Credit Union Lending Strategies in 2026: Insights from Rising Delinquencies and Evolving Debt Perceptions

By Devon Kinkead

As we look ahead to 2026, credit unions face a dynamic lending landscape shaped by economic pressures, shifting consumer behaviors, and regulatory demands. At Micronotes, we’ve long championed data-driven prescreen marketing to help financial institutions like credit unions optimize their lending portfolios. Drawing from recent research on debt perceptions and alarming trends in subprime auto loan delinquencies, this blog explores strategic imperatives for credit unions to thrive. By leveraging AI-powered personalization and precision targeting, credit unions can mitigate risks, boost member engagement, and drive sustainable growth—all while aligning with their member-centric missions.

The current economic climate underscores the urgency for adaptive strategies. A recent analysis highlights that subprime auto loan delinquencies hit a record 6.65% in late payments of 60 days or more, the highest since the early 1990s, according to Fitch Ratings. This surge coincides with Tricolor Holdings’ bankruptcy, signaling vulnerabilities in high-risk lending. Factors like skyrocketing average new car prices—around $50,000—and elevated interest rates have amplified financing costs, outpacing inflation in other sectors. As MIT Sloan’s Christopher Palmer notes, this reflects broader strains on vulnerable households, where auto loans serve as economic lifelines for commuting, education, and family needs. Unlike mortgages or student loans, car repossessions can occur swiftly, exacerbating financial distress.

Yet, this isn’t a repeat of the 2008 subprime mortgage crisis. Auto loans represent a fraction of total debt—mortgage balances are nearly eight times larger, per the New York Federal Reserve—and institutions aren’t as exposed. Delinquencies haven’t yet translated into widespread defaults or bankruptcies, as Moody’s Analytics observes. Still, for credit unions, these trends signal a need to refine lending approaches, particularly in auto, personal, and home equity lines of credit (HELOCs).

Complementing this is emerging research on Americans’ views of debt, which reveals moral dimensions influencing financial decisions. A study from MIT Sloan, involving surveys and experiments, shows that attitudes toward debt are deeply tied to personal moral values—such as duty and honor in repayment—rather than just financial literacy. Respondents prioritize moral considerations in hypothetical scenarios, suggesting that debt aversion stems from ethical frameworks. This has profound implications: Credit unions must craft lending products and marketing that resonate with members’ values, framing offers as tools for financial empowerment rather than burdensome obligations.

In 2026, we anticipate a bifurcated credit market—the “barbell effect”—where super-prime originations grow by over 9% and subprime by 21%, while prime segments shrink. Credit unions, with their community roots, are uniquely positioned to navigate this. At Micronotes, our Prescreen platform processes over 230 million credit records weekly, enabling automated prescreen campaigns that target both ends of the spectrum. For super-prime members, strategies focus on refinancing and cross-selling wealth products, like consolidating high-interest credit card debt into lower-rate personal or home equity loans. Imagine offering a member a personalized deal: “Reduce your 19.89% credit card rate to 8.64% with our consolidation loan—saving $X monthly.” Such precision lifts conversions and fosters loyalty.

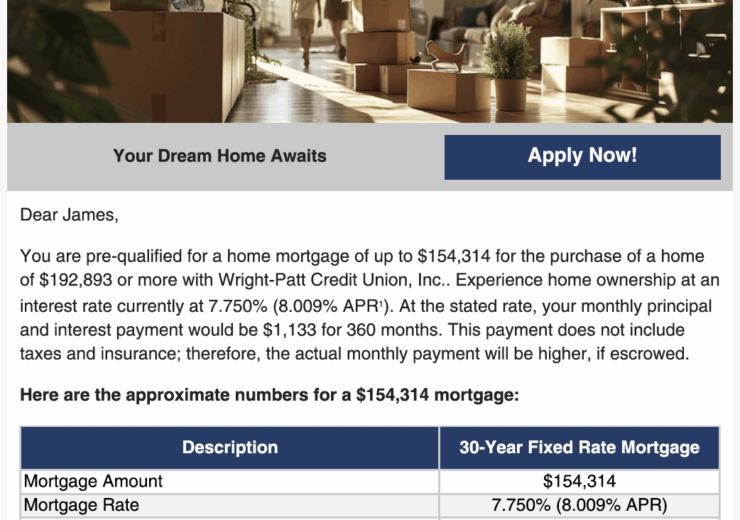

For subprime segments, risk management is paramount amid rising delinquencies. Prescreening allows credit unions to assess risks granularly, offering graduated products like secured loans or debt consolidation tied to financial coaching. This mirrors initiatives like Wright-Patt Credit Union’s homeownership program, where prescreen identified 172,328 mortgage candidates, unlocking $35.8 billion in potential volume, plus cross-sell opportunities in auto refinances ($1 billion) and HELOCs ($6.7 billion). By integrating behavioral triggers—such as proximity to branches for trust-building—campaigns can achieve net negative acquisition costs, turning marketing into a profit center.

Compliance remains a cornerstone, especially with AI’s role in lending. The Fair Credit Reporting Act (FCRA) demands auditability, and variables like credit scores or ZIP codes can introduce bias. Micronotes embeds compliance from campaign design, using pre-launch checks and post-campaign analytics to detect disparate impacts. This feedback loop—measuring response rates, cost per acquisition (CPA), and profitability—enables continuous optimization.

Speed and agility will differentiate winners. Drawing from agile frameworks like those at Standard Chartered, credit unions should adopt rank-ordered backlogs for prescreen campaigns, limiting work-in-progress to slash cycle times. Weekly huddles and improvement sessions can address bottlenecks, from data inputs to creative launches. This ensures offers reach members amid fast-moving events, like interest rate shifts or economic dips.

Branches, too, evolve in this strategy. Our data shows HELOC conversions plummet beyond 15 miles from a branch, underscoring proximity’s role in high-stakes decisions. A hybrid model—geo-weighted digital marketing for distant members, in-person reassurance for locals—maximizes impact.

Looking to HELOCs as a growth area, 2026 strategies should monitor “market signals”—debt pattern drifts, competitor encroachments, or prime underperformance. Persistent digital presence, rapid response protocols, and differentiated value (e.g., flexible draw periods) will capture share. Micronotes’ platform facilitates this by offering extensive post campaign analytics to scaling successes and delete failures.

Ultimately, credit unions’ lending success in 2026 hinges on precision over scale. Community institutions leverage trust and agility to outmaneuver big banks, achieving 3.2x revenue from primary relationships. By embracing prescreen marketing, credit unions can align with members’ moral views on debt—positioning loans as honorable paths to stability—while sidestepping delinquency pitfalls. At Micronotes, we’re committed to empowering this shift, helping you turn data into meaningful member outcomes. As delinquencies remind us, proactive, personalized strategies aren’t just smart—they’re essential for resilient growth.