Debunking Prescreen Marketing Myths: Runaway Application Volumes

By Devon Kinkead

Myths often cloud the reality of banking operations when new technologies enter the market. One such myth is the belief that bankers will be overwhelmed by the loan volume generated from prescreen marketing campaigns. However, this misconception doesn’t hold up under scrutiny.

Prescreen Marketing Campaigns

Prescreen marketing campaigns are a proven market share and wallet share growth strategy with an average volume of 400MM prescreen offers mailed per month, or more than one for each adult in the U.S., and an important steady source of revenue for the US Postal Service. These firm offers of credit are used to identify and credit prequalify potential borrowers. These campaigns involve sending financially personalized, FCRA compliant, pre-approved loan offers to individuals who meet specific credit criteria. The goal is to drive prequalified loan applications and increase the institution’s lending portfolio.

The 17-Week Window

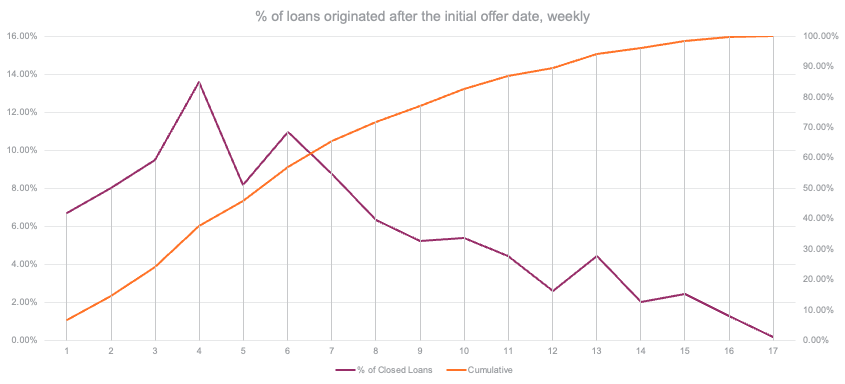

A critical aspect of prescreen marketing campaigns that is often overlooked is the extended loan application and processing window. Contrary to the concerns among financial institutions that are new to prescreen marketing, loan applications from these campaigns are not received all at once. Instead, applications and loans are typically spread out over a 17-week period following the initial mailing as shown in figure 1. This reality significantly reduces the potential for overwhelming loan volumes. For example, about the same number of loans are closed in weeks 7-8 as are closed in week 1, or about 7% of the total number of loans closed.

Figure 1 – Loan volume over time following campaign start, $1B community financial institution.

Antiquated Loan Application and Processing Systems

Even financial institutions with antiquated loan application and processing systems can handle an uptick in loan volume over the course of 4+ months from fully qualified borrowers. With 85-90% of applications funded, this is highly productive work.

Conclusion

The notion that bankers can’t handle the loan volume associated with prescreen marketing campaigns is a myth that doesn’t hold up to scrutiny. The 17-week closed loan window combined with good estimates of total expected loan volumes, by type, from the Micronotes Growth Analysis make the leap to automated prescreen marketing for market share and wallet share expansion more like a stair-step.

Prescreen marketing, historically used by large banks, fintechs and credit unions due to its cost and complexity, is now available to all community financial institutions that want to grow market share and wallet share in their operating footprint with steady and manageable loan volume growth.