When Members Save More and Borrow Less: Turning Trends Into Strategic Opportunity

By Devon Kinkead

A Prescreen Marketing Perspective on Credit Union Performance

The latest Q3 2025 data from Callahan & Associates reveals a fascinating paradox facing credit union executives: members are demonstrating remarkable financial discipline by growing their share balances at rates we haven’t seen in years, yet loan growth continues to decelerate. For leaders committed to both member financial wellness and institutional sustainability, this presents a strategic inflection point that demands a more sophisticated approach to member engagement.

Understanding the Current Landscape

The numbers tell a compelling story. Membership growth ticked up to 2.2% in Q325, reversing years of deceleration. Share portfolios grew by over $64 billion in Q125 alone, with regular shares and share drafts leading the charge. Members aren’t just parking money in certificates anymore—they’re building accessible emergency funds, signaling heightened awareness of economic uncertainty.

Meanwhile, loan originations are rising, particularly in real estate where rate-sensitive borrowers are responding to Federal Reserve cuts. Yet total loan growth remains modest. The average member relationship shows members holding more in shares while borrowing selectively. Delinquency, while rising seasonally, remains manageable, with the coverage ratio holding steady at 164%.

Perhaps most encouraging for the bottom line: net interest margins hit 3.38%, the highest this millennium, creating operational flexibility that forward-thinking institutions can deploy strategically.

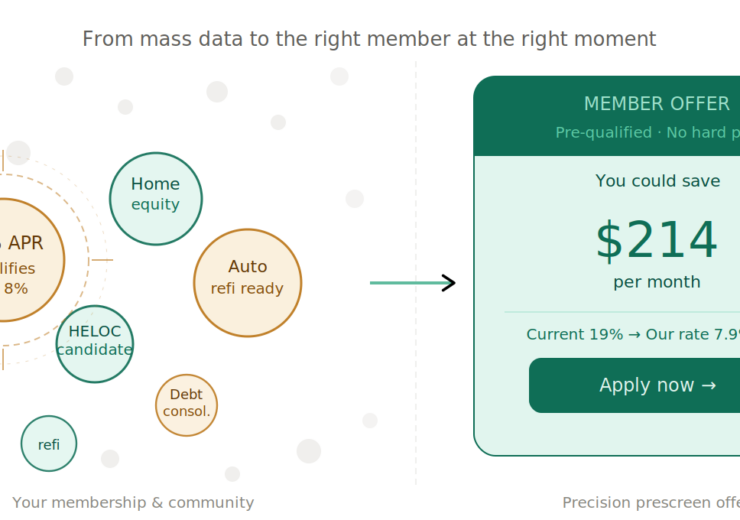

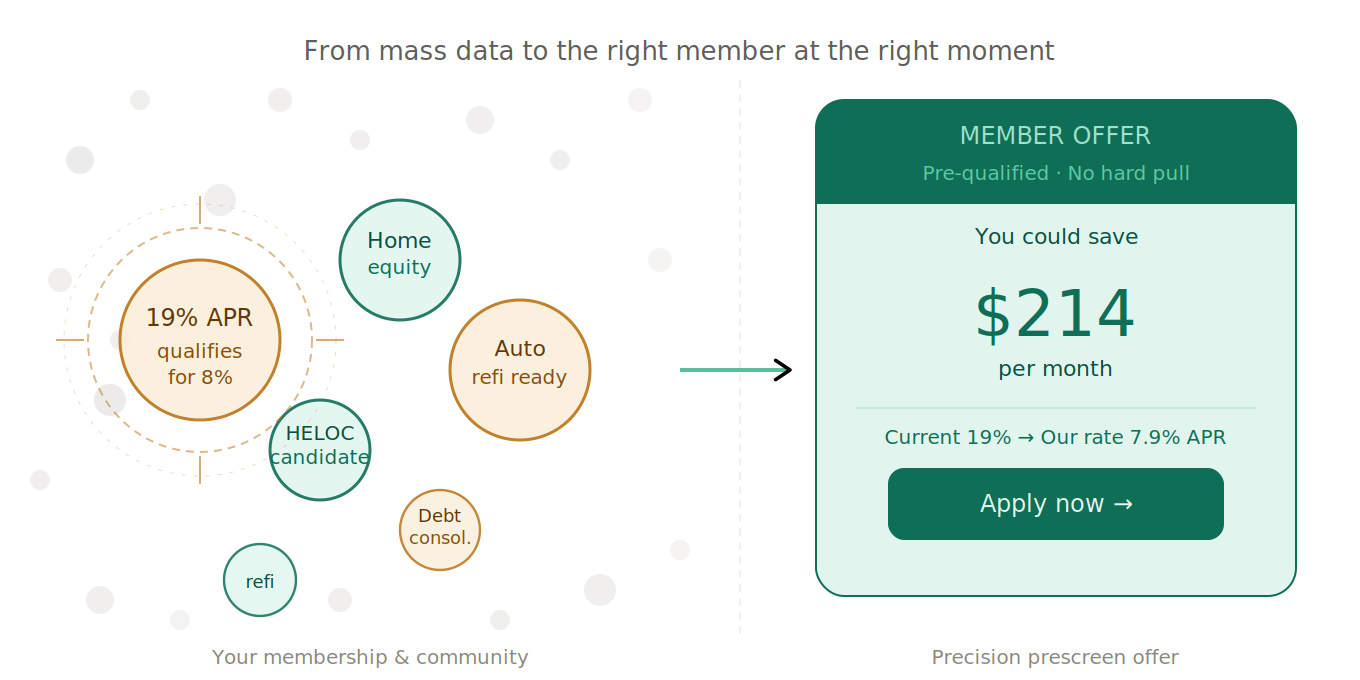

The Precision Opportunity Hidden in Plain Sight

Here’s what the aggregate data doesn’t show: within your membership and surrounding community sit thousands of individuals who would benefit from credit union lending but haven’t been presented with the right offer at the right time. They’re paying 19% on credit cards when they qualify for 8% consolidation loans. They’re sitting on home equity while struggling with high-interest debt. They’re financing vehicles at captive lenders when your rates would save them hundreds monthly.

The TrendWatch data showing members prioritizing liquidity and accessible savings reinforces an important insight: members aren’t opposed to borrowing—they’re being selective, prudent, and waiting for offers that genuinely serve their interests. This is precisely where automated prescreen marketing transforms industry-wide trends into institutional advantage.

From Broad Campaigns to Surgical Precision

Traditional marketing approaches—batch-and-blast campaigns with generic rate messaging—cannot capture the nuance this environment demands. When loan growth is slowing industry-wide but certain segments show strong conversion potential, success requires identifying exactly who qualifies, for what products, at what specific terms.

Consider the opportunity in debt consolidation alone. Members carrying high-interest balances who now qualify for better terms represent immediate value creation—for them through monthly savings, for your institution through quality loan growth. But finding them requires processing millions of credit records against your specific underwriting criteria, generating compliant firm offers, and delivering personalized communications that show exact dollar savings.

The credit unions capturing market share today aren’t waiting for members to walk through the door asking about refinancing. They’re proactively identifying opportunities and presenting compelling, pre-qualified offers before competitors do.

Aligning Growth Strategy with Member Wellness

The beauty of precision prescreen marketing is how naturally it aligns with credit union mission. When you identify a member paying excessive interest and offer them a consolidation loan at half the rate, you’re not pushing product—you’re genuinely improving their financial health. When you reach a prospect who qualifies for a HELOC to consolidate debt, you’re potentially transforming their monthly cash flow.

This matters especially in what economists describe as a K-shaped economy, where some Americans thrive while others struggle with inflation in essentials like food, energy, and housing. Credit unions exist to serve members of modest means. Precision targeting ensures your outreach reaches those who would benefit most, not just those most likely to respond to generic advertising.

The Path Forward

The Q3 2025 data confirms what many executives sense intuitively: the environment rewards institutions that can move quickly, target precisely, and demonstrate genuine value to members. With margins at historic highs, credit unions have the financial flexibility to invest in capabilities that will define competitive positioning for years to come.

The question isn’t whether members want to borrow—rising originations in rate-sensitive categories prove they do when the terms make sense. The question is whether your institution can identify qualifying individuals, reach them with compliant and compelling offers, and close loans before competitors capture the opportunity.

In a market where members are demonstrating financial prudence by saving more and borrowing selectively, the institutions that thrive will be those that respect that prudence by presenting genuinely beneficial opportunities rather than generic rate advertisements. Automated prescreen marketing provides the mechanism to do exactly that—at scale, with speed, and in full regulatory compliance.

The trends are clear. The tools exist. The margin advantage provides runway. What remains is the strategic decision to move from reactive, broad-based marketing to proactive, precision-targeted member engagement. For credit unions committed to both mission and sustainability, that decision has never been more timely.

See who you can help in your backyard here: https://micronotes.ai/growth-opportunities-analysis/