When Purpose Meets Precision: How Wright-Patt Credit Union Is Turning 172,000+ Opportunities Into Homeownership Reality

By Devon Kinkead

When Savana Morie’s recent article in Credit Unions Magazine highlighted Wright-Patt Credit Union’s transformative Pathways to Homeownership initiative, it struck a particularly personal chord for me. Having spent the first 18 years of my life in Dayton, Ohio, I’ve witnessed firsthand the challenges facing Northwest Dayton—the very communities Wright-Patt is working to revitalize.

But beyond the personal connection, this story represents something even more powerful: the intersection of mission-driven purpose and data-driven precision that defines modern credit union growth.

The Challenge Hidden in Plain Sight

Wright-Patt Credit Union ($9.3B, Beavercreek, OH) has emerged as one of the two largest purchase-money lenders in the Dayton area, with more than half their mortgages going to first-time buyers. As President and CEO Tim Mislansky shared with Morie, “Affordable homeownership is one of the keys to financial success. When we can help members become homeowners, we can help them build wealth, strengthen families, and create lasting communities.”

That commitment is admirable—and it’s backed by a $1.3 million investment from the WPCU Sunshine Community Fund to construct 30 new homes in Northwest Dayton over the next three years. But here’s the question every mission-driven credit union must ask: How do you find the right people to fill those homes?

The Data Behind the Dream

This is where prescreen marketing transforms theory into impact. Our recent (Sep 2025) Growth Opportunities Analysis for Wright-Patt Credit Union revealed something remarkable:

Within just 5 miles of Wright-Patt’s 40 branches, there are 172,328 credit-qualified individuals ready for mortgage opportunities—representing a potential loan volume of $35.8 billion.

Let me put that in perspective. While Wright-Patt is building 30 homes over three years through their Pathways initiative, there are over 172,000 qualified mortgage candidates already living in their branch network footprint. These aren’t random names—these are real people who:

- Have FICO scores between 680 and 850

- Have demonstrated responsible credit behavior with no current delinquencies

- Meet industry standard underwriting criteria (below)

- Live within a short drive of a Wright-Patt branch

- Are currently without a mortgage or are first-time homebuyers

| Criteria Definition | Rule Summary |

| FICO Score | Between 680 and 850. |

| Total number of debt counseling trades excluding collections | Equal to 0. |

| Total number of trades presently 30 or more days delinquent or derogatory excluding collections | Equal to 0. |

| Total number of trades ever 30 or more days delinquent or derogatory occurred in the last 12 months including collections | Equal to 0. |

| Total number of trades ever repossessed | Equal to 0. |

| Number of months since the most recent trade ever charged-off including indeterminates | No charged-off trades ever. |

| Total number of public record bankruptcies | Equal to 0. |

| Total number of trades excluding collections and student loans including indeterminates | Greater than or equal to 3. |

| Number of months since the oldest trade was opened excluding collections and student loans including indeterminates | Greater than 36. |

| Total number of non-medical collection trades | Equal to 0. |

| Total balance on medical collections | Less than or equal to $2,000. |

| Total number of first mortgage trades ever foreclosed including settled first mortgages | Equal to 0. |

Not all 172,328 will qualify for enough of a loan to meet market home prices so, the credit union should take market prices into account when designing the prescreen campaign ensuring that any such policy does not create a disparate impact under the ECOA or Fair Housing Act.

From Mass Marketing to Mission Alignment

Traditional mortgage marketing casts a wide net and hopes for the best. Prescreen marketing does something fundamentally different: it identifies individuals who already qualify for your specific lending criteria before you ever reach out.

For Wright-Patt’s Pathways to Homeownership initiative, this precision matters even more. Director of Community and Social Impact Ivy Glover told Morie that the program includes a five-week homeownership readiness program, one-on-one coaching, and financial education sessions. That’s a significant investment of time and resources—which makes targeting the right candidates from the start absolutely critical.

“We didn’t just cut a check,” Glover explained. “We committed to making homeowners.”

The Micronotes Advantage: Turning Data Into Opportunity

Our Automated Prescreen™ platform analyzed 1,809,213 Experian records within 5 miles of Wright-Patt’s branch locations. After applying Wright-Patt’s underwriting criteria, we identified 723,188 qualified prospects across all loan categories.

For mortgage opportunities specifically, here’s what we found:

- 172,328 qualified mortgage candidates

- $35.8 billion in potential loan volume

- Average loan qualification: $154,314

- All candidates living within a 5-mile radius of 40 branches across 182 zip codes

Once the program is executed, each prospect receives a personalized, firm offer of credit—not a generic “you might qualify” message, but an actual pre-qualified offer with specific loan amounts, rates, and monthly payments based on their individual financial profile.

Bridging the Education Gap

One of Glover’s key insights in the article particularly resonates with our approach: “I wish we’d started the education piece sooner.”

This is where prescreen marketing creates a natural bridge between acquisition and education. When you reach a qualified prospect with a specific, personalized offer, you’re not starting a conversation from scratch—you’re answering a question they may have already been asking themselves: “Can I afford a home?”

For Wright-Patt’s target demographic in Northwest Dayton—where over 70% of residents rent and more than 40% are housing-cost burdened—seeing a concrete, qualified mortgage offer can be the catalyst that transforms “someday” into “now.”

The Ripple That Could Become a Wave

Glover shared with Morie: “I tell my team all the time: Every drop makes a ripple, but some make a much bigger one. This is a big ripple moment.”

She’s absolutely right. But imagine if Wright-Patt could systematically identify and reach every qualified mortgage candidate in their branch network? What starts as a ripple could become a genuine wave of homeownership transformation.

Our analysis reveals opportunities across multiple product categories that support the journey to homeownership:

- 104,890 qualified personal consolidation loan prospects ($1.4B volume) to help clear high-interest debt

- 53,010 HELOC/HELOAN consolidation opportunities ($6.7B volume) for existing homeowners looking to refinance

- 47,764 auto loan refinance prospects ($1B volume) to free up monthly cash flow

Each of these products plays a supporting role in the homeownership journey—helping members improve their debt-to-income ratios, build credit, and position themselves for mortgage qualification.

A Personal Note on Coming Home

As someone who grew up in Dayton, I’ve watched neighborhoods transform—sometimes for better, sometimes for worse. The 2019 Memorial Day tornadoes that sparked the original Pathways to Homeownership initiative devastated communities I knew well.

What Wright-Patt is doing goes beyond lending. As Glover notes, “My teacher lived down the street; my doctor was two blocks over. One of the goals is to restore that sense of community and accountability where people know their neighbors and look out for one another.”

That’s the kind of community impact that makes this work meaningful. And data-driven prescreen marketing is the bridge that connects mission to execution—ensuring that every qualified member who could benefit from these programs actually knows they exist and can access them.

The Path Forward

Wright-Patt still needs to raise an additional $2.75 million to complete Phase III of their housing initiative. But as Mislansky told Morie, “We believe this, along with continued fundraising and collective storytelling from all the partners, will lead to the additional funding needed to complete the next phases.”

Perhaps, if Wright-Patt can help more first-time homeowners at lower cost, it can funnel some of those savings into Phase III.

That storytelling becomes even more powerful when backed by data. When donors and partners can see not just 30 new homes, but 172,328 qualified opportunities waiting to be realized, the vision expands from a project to a movement.

Making Every Connection Count

Wright-Patt’s Housing Collective represents exactly the kind of cross-departmental, mission-driven thinking that defines successful credit unions today. But mission without mechanism is just aspiration.

Prescreen marketing provides that mechanism—the ability to:

- Identify qualified prospects with surgical precision

- Reach them with personalized, firm offers of credit

- Convert interest into applications

- Learn from post-campaign analytics and improve next campaign performance

- Scale successful programs across your entire branch network

For a credit union committed to making “more than half” of their mortgages to first-time buyers, the ability to systematically identify and reach 172,328 qualified mortgage candidates isn’t just a nice-to-have—it’s a strategic imperative.

The Bottom Line

Wright-Patt Credit Union is doing exactly what credit unions were founded to do: serving people of modest means and rebuilding communities from the inside out. Their $1.3 million investment, their five-week education program, their partnership with community organizations—all of it represents the best of the credit union movement.

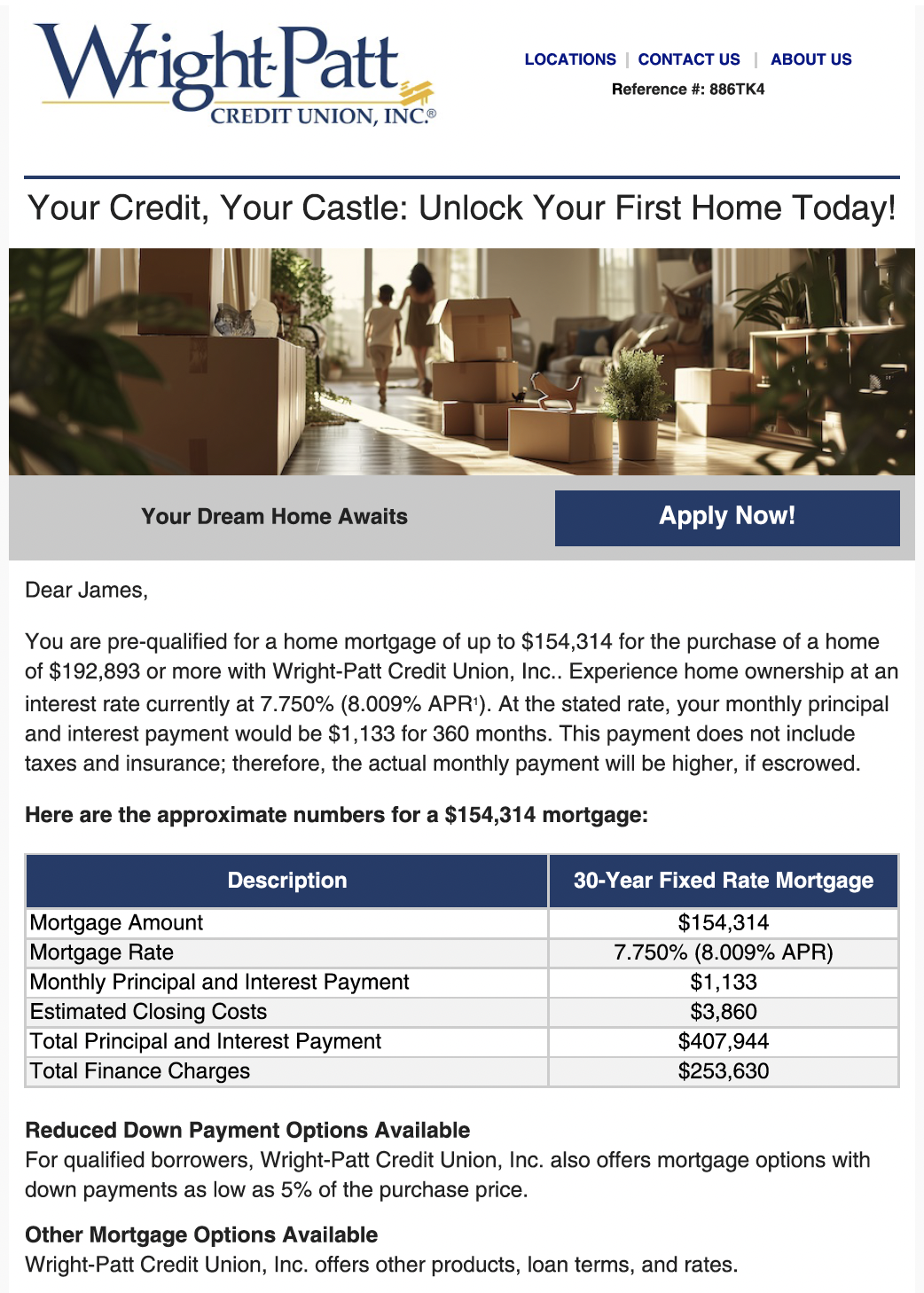

Micronotes’ role is to ensure that this incredible work reaches everyone who could benefit from it. That James, the single father in Northwest Dayton who’s been renting for years discovers he actually qualifies for a $154,000 mortgage. That the young couple making ends meet learns they could consolidate their high-interest debt and free up $261 per month. That the family dreaming of homeownership finds out their dream is actually within reach.

As Mislansky concluded in his conversation with Morie: “We believe this program can change lives, revitalize communities, and demonstrate what’s possible when mission-driven organizations work together.”

With 172,328 qualified opportunities waiting within just 5 miles of Wright-Patt’s branches, the question isn’t whether they can change lives—it’s how many, and how fast.

Start your credit marketing journey today