Scaling the Personal Touch: Data-Driven Lending That Feels Human

A member walked into a Logix Federal Credit Union branch recently, confused about her account. She had been experiencing memory challenges after losing both her daughter and her mother. The employee didn’t rush her through the transaction. Instead, she patiently walked through every detail, reassured the member she had nothing to be ashamed of, and listened as the member shared photos of her loved ones. Later, the employee sent a necklace with pendants bearing the initials of the member’s daughter and mother.[1]

After a decade of working with Logix, we can say, Micronotes loves the Logix team and this story isn’t surprising.

This is the kind of story that defines community financial institutions. It’s also the kind of story that keeps executives up at night—because moments like these are beautiful, brand-defining, and almost impossible to replicate at scale.

The Scalability Problem With Relationship Banking

Community banks and credit unions have long claimed relationship banking as their competitive moat. And they’re right to do so. According to a 2023 study by Rivel Banking Research, 67% of consumers who switched from a megabank to a community institution cited “personal service” as the primary driver.[2]

But here’s the uncomfortable truth: these relationship-defining moments are random. They depend on which member walks into which branch and encounters which employee on which day. Your best frontline people create magic. Your average ones process transactions. And your digital channels? They often feel like they belong to an entirely different institution.

Meanwhile, the outbound marketing most FIs deploy actively undermines their relationship positioning. Generic credit card offers. Mass-mailed auto loan promotions with no relevance to the recipient’s actual financial situation. According to the Data & Marketing Association, the average response rate for direct mail across financial services hovers around 2.7%.[3] That means 97% of recipients experience your brand as noise.

What “I See You” Looks Like in Lending

The Logix story works because the employee recognized the member’s specific circumstances and responded with unexpected care. She didn’t offer a generic solution. She noticed, she listened, and she acted on what she learned.

Prescreen marketing—when executed with precision—can replicate this dynamic digitally. The FCRA allows financial institutions to use credit bureau data to extend firm offers of credit to consumers who meet specific criteria.[4] Most FIs use this capability crudely: pull a list, mail an offer, hope for the best.

But the same data that enables a firm offer also enables genuine relevance. Consider the difference:

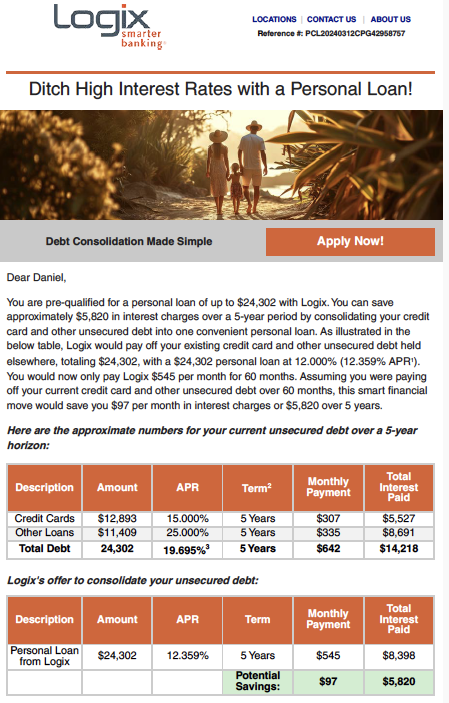

- Generic approach: “You’re pre-approved for a personal loan up to $15,000!”

- Precision approach: A debt consolidation offer sent specifically to members carrying high-interest balances across multiple cards, with messaging that includes the exact savings for that member available by refinancing that debt at a lower rate. For example:

The second approach signals something powerful: We see your situation, and we’re here to help. That’s the lending equivalent of noticing someone is struggling and proactively offering assistance before they ask.

The Data That Enables Institutional Empathy

Credit data reveals more than creditworthiness. It reveals financial circumstances—and by extension, human circumstances. A member with a thin credit file but strong payment history and rising home equity might be a first-generation homeowner building wealth carefully. A member with a sudden spike in revolving utilization might be navigating an unexpected financial shock.

When you segment prescreen campaigns around these signals, you stop sending offers and start sending solutions. The Federal Reserve’s 2023 Survey of Consumer Finances found that 37% of American households carry credit card debt, with a median balance of $5,700 among those with balances.[5] For credit unions specifically, NCUA data shows that as of Q3 2024, credit card balances at federally insured credit unions reached $97.2 billion.[6]

These aren’t just statistics. They represent members who could benefit from a well-timed consolidation offer, a balance transfer opportunity, or a personal loan that reduces their monthly burden. The question is whether your institution will reach them first—or whether a fintech or megabank will.

From Junk Mail to Relationship Touchpoint

The transformation requires three shifts in how community FIs approach prescreen marketing:

- From volume to precision: Smaller, highly targeted campaigns outperform mass mailings. When offers align with recipient circumstances, response rates soar.

- From product-push to problem-solve: Lead with the member’s pain point, not your product features. “You’re overpaying $97/mo.”

- From one-touch to multi-channel: Direct mail remains effective, but combining it with digital retargeting and personalized follow-up multiplies impact. Members increasingly expect consistency across channels.

The Community FI Advantage—If You Claim It

Megabanks have data scientists and marketing automation platforms. Fintechs have agility and digital-native infrastructure. But community banks and credit unions have something neither can replicate: an authentic commitment to member wellbeing and decades of local trust.

The Logix employee didn’t send that necklace because a playbook told her to. She did it because the Logix culture—its WOW Program—empowered her to act on genuine care.[1] Data-driven prescreen marketing doesn’t replace that culture. It extends it. It ensures that the same institutional empathy your best employees demonstrate in person reaches members who never walk into a branch.

The strategic question for community FI leaders isn’t whether to invest in prescreen capabilities. It’s whether you’ll use those capabilities to reinforce your relationship positioning—or undermine it with generic offers that feel indistinguishable from what Chase sends.

Your members don’t want more mail. They want to feel seen. The technology exists to deliver that experience at scale. The remaining variable is strategic intent.

Start your journey today with a near-branch growth analysis here.

References

- A Reminder They’re Never Forgotten – CreditUnions.com

- Rivel Banking Research – Consumer Banking Insights

- Data & Marketing Association Response Rate Report

- Fair Credit Reporting Act – Federal Trade Commission

- 2023 Survey of Consumer Finances – Federal Reserve

- NCUA Quarterly Credit Union Data Summary